According to eMarketer the Online Video Ad Spend is at USD 4.14 billion likely to reach USD 7 billion by 2015. Forrester expects spending on all online video advertising to hit nearly $3.6 billion in 2013, increasing to $4.6 billion in 2014. Between 2011 and 2017, online video ad revenue across PC and mobile platforms will experience a 26% compound annual growth rate (CAGR), faster than any other digital medium like mobile or social.

In contrast, the US display ad business is growing slower, with static image revenues expected to decline overall and rich media placements only growing by 16%. Brand marketers are attracted by the opportunity to provide richer advertising experiences using online video, particularly as buying based on targeted audiences and other placement attributes gains greater traction in this more visual and engaging format.

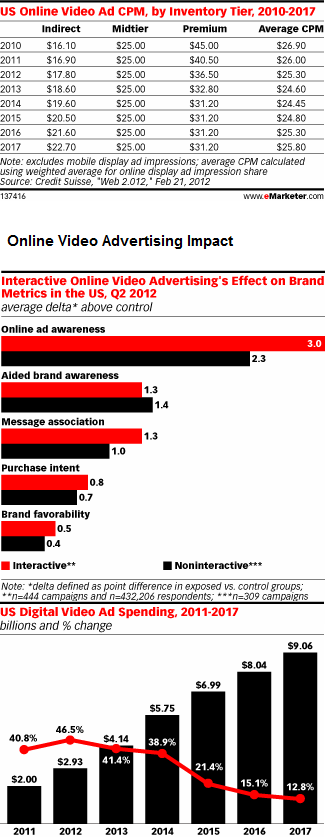

Interactive Online Video Advertising has a positive effect on Brand Metrics right from increasing awareness to Brand Favoribilty.

As online video has grown, RTB inventory and revenue have grown faster than the overall video market as a buying mechanism for acquiring inventory. Between 2011 and 2014, RTB video spend will grow at a blistering pace of a 57% CAGR. Spend using this mechanism is forecast to reach $686 million in 2013 and cross the billion dollar threshold in 2014, when spend will reach $1.14 billion. RTB also outpaces growth of overall video when it comes to impressions, with a 61% CAGR.

Programmatic Buying and RTB will continue to provide video advertiser buying efficiencies as digital engagement grows significantly through the buyer journey. RTB will become Real-time buying as audience targeting and automated placement of direct buying continues to gain prominence. Brand marketers continue to look at Advertising in a more visually engaging and interactive formats and media buying based on targeted audiences to provide a richer experience.

Google conducted a study with Automobile buyers and looked at more than 10,000 Purchasers Digital Paths, 1000 Online Surveys and ethnography participants.

The key Findings are:

1. Memorable Brand Engagement is one of the key influencers in the Path-to-Purchase.

2. Younger audiences look at more than four brands in their decision journey.

3. Video Websites and Social Media Websites are a third of all digital tools for researching Products.

4. Daily usage of Mobile Devices with the Shoppers is higher than 70%.

5. 29% Shoppers discovered Brands they were not aware of.

6. For mobile shoppers considering more than four brands, Social Sharing is an important part of the purchase process as 51% sent pictures of cars and 44% used comparison tool while at the dealership and 49% looked at consumer reviews.

7. Open-minded shoppers became engaged owners with digital engagement going up by 4X.

Source: RTB Powers the Rapid Growth of Online Video, Forrester and eMarketer-Online Video Advertising Moves from Front and Center, Google – Brand choice on the new vehicle path to purchase